the week we cut twelve tools to one.

Affinity, DocSend, Carta, Diligent, Excel, Notion. What it looked like to replace a typical fund's tool stack with VCOS in five days.

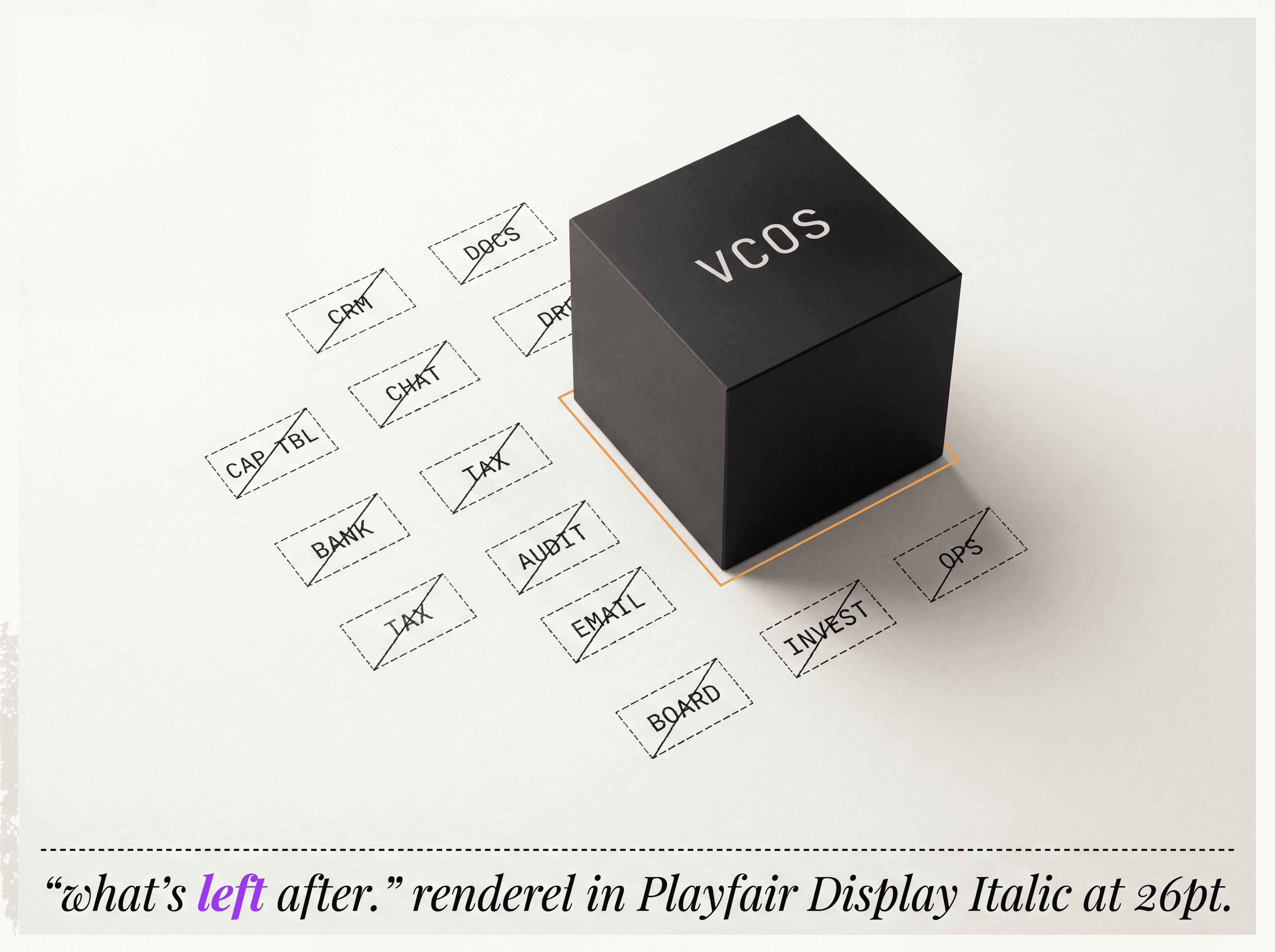

On a Monday in March, the operations partner at a Series A fund printed her tool stack onto a sheet of paper and laid it on the table at the partner meeting. Twelve line items. Affinity for the CRM. DocSend for deck sharing. Carta for the cap table. Diligent for board materials. Excel for the model. Notion for the wiki. Slack, Gmail, DocuSign, Box, QuickBooks, and a fund admin portal whose name she had to look up. The annual cost was sixty-three thousand dollars before seats. The implementation, training, and integration tax was harder to add up.

The fund's first AGM was in eight weeks.

the spreadsheet.

She had three motivations. The first was money, but she would tell you it was not really about money. Sixty-three thousand a year is a rounding error against a fund's management fee. The second was data fragmentation. Affinity knew about the deals, Notion knew about the diligence, Carta knew about the cap table, and none of them knew about each other. The third was the AGM. She had spent the previous AGM cycle assembling LP-ready numbers from six different exports. She did not want to do that again.

We met her on Thursday. By the next Friday, the fund was running on VCOS.

monday.

Monday was the audit day. We read every export from every tool, traced where the same deal was represented in three places, and built a map of the canonical record. Where Affinity called something a Series A in fintech, DocSend called it a stage one finserv, and the model called it FinTech II 2026 vintage, we collapsed those into a single record with the right metadata.

Monday was the boring day. It was also the day the partner watched her data collapse into a single graph and said the only useful thing anyone has ever said about migrations. I see what we have now.

tuesday through thursday.

Tuesday and Wednesday were import days. Cap tables, deal flow, fund admin records, every LP commitment, every founder relationship, every quarterly report. By Wednesday afternoon Vista had its first real working dashboard. By Thursday morning the team was running queries that had been impossible the week before. Show me every deal that came through a warm intro from one of our LPs in the last two years. Thirty-one results in two seconds. The previous version of that query had been a partial answer assembled from three exports over half a day.

i see what we have now.

friday.

Friday was the kill day. We watched the partner cancel eleven subscriptions. The twelfth, the fund admin portal, was already on a three-month termination clock for compliance reasons. By the following Friday it would also be gone.

The fund did not get faster overnight. It got slower for two days while the team learned the new shapes. Then it got dramatically faster. Diligence cycles dropped from twelve days to four. The first capital call from VCOS went out the following month and closed without a single LP question. The AGM in week eight ran on a single set of numbers, generated thirty minutes before the meeting started.

What does a fund do with sixty-three thousand dollars and four reclaimed weeks per year. The fund we worked with redirected the budget to a temporary analyst hire who built the next two years of investment-thesis research. The reclaimed time went where it always should. To founders, to conviction, and to the work of being a partner.